|

|

|

|

|

|

Grab Your Rod & Reel, The Bees Are Biting

By Morgan Christen

CFA, CFP, CDFA, CEO and CIO

Welcome,

Believe it or not, in May of 2022 California, ruled that bumblebees are considered fish.

Should we chalk it up to crazy California, or par for the 2022 course? It may sound fishy (sorry) but it was done to protect bees under the Endangered Species Act.

|

|

|

|

|

|

|

Beyond bees, 2022 ended up being quite an eventful year. The first trading day of 2022 was an historic day as Apple became the first company in history to reach a valuation of $3 trillion (yes, trillion).

Unfortunately for Apple and the other stock/bond markets, the next day the Fed minutes revealed Fed officials were on board to quickly reduce their asset purchase program. The Nasdaq ended down more than 3% that day.

|

|

|

Then came June when Jay Powell and company went big and started their first 75 basis point rate hike, ending the year in the 4.25% - 4.50% range.

These rate increases caused havoc in the overvalued technology space.

To name a few pinged by rates...

|

Tesla off nearly 73%

Meta off 64%

Netflix 51%

Amazon nearly 50%

Alphabet 39%

Apple off 26% for the year

If you are counting, the loss for Tesla is around $720 billion of shareholder value in 2022.

|

|

|

|

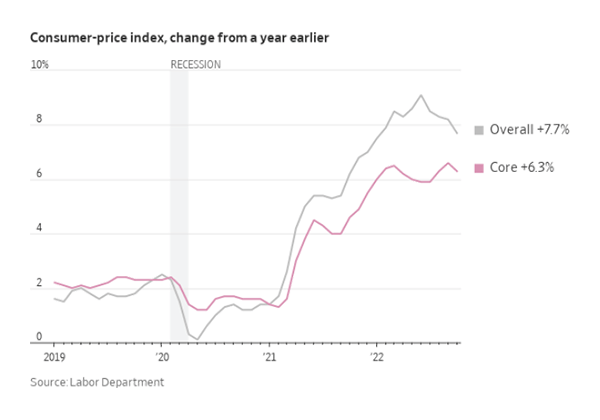

The main topic of the year in markets was interest rates, and where the Fed would take them. That narrative was driven by an inflation rate that hit its highest level in 40 years. But don't tell that to Matchbox.

Crypto fell as FTX and other platforms imploded. For some color, there are over 9,300 cryptocurrencies in existence versus 180 government-sponsored currencies in the world. That was bound to correct.

|

|

|

|

|

Non-financial topics included the invasion of Ukraine, Wordle, new viruses such as Monkeypox and RSV. How do you pronounce Qatar?

We had a couple of GOATs retire, Serena Williams and Tom Brady (but only for 40 days). We said goodbye to a Queen, a Secretary of State, a Golden Girl, Danny Tanner, the Aflac duck, a Foo, Meat Loaf and Sandy.

|

|

|

|

|

|

|

Stocks

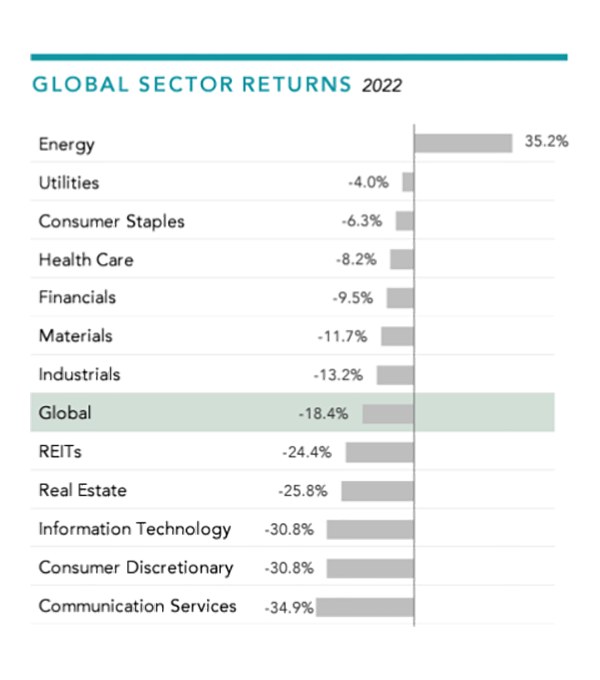

Stocks managed to register their worst year since 2008. You can put much of the blame on the Fed and their actions to curb inflation. But you can also blame very lofty valuations that needed to compress.

The hottest sectors took the greatest hit. You will see in the global sector chart, communications services at the bottom. Who fits into that sector? Alphabet (Google), Meta (Facebook), and Roku, to name a few.

|

|

|

|

|

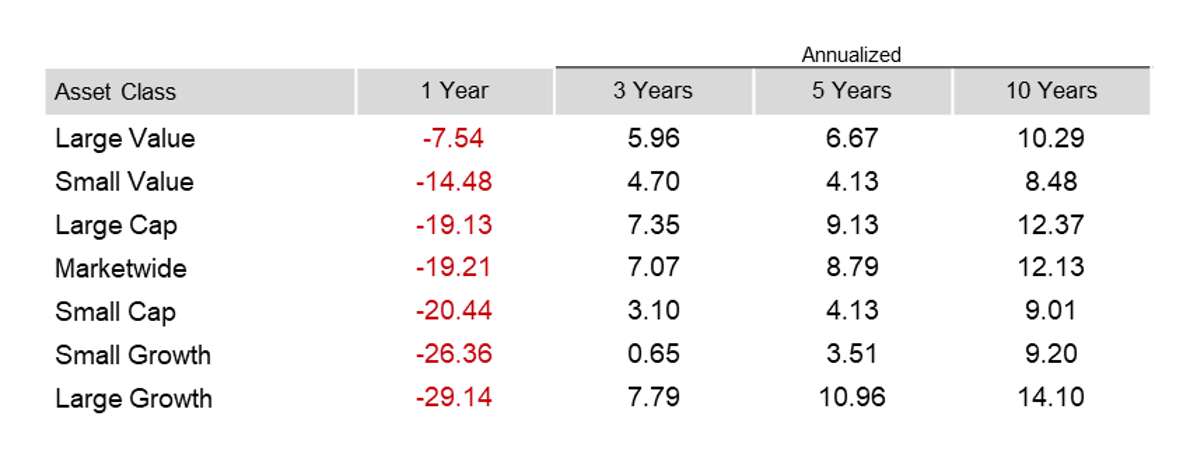

The major indexes also had varied performance as the tech heavy NASDAQ was off 33% for the year followed by the modestly tech heavy S&P 500 suffering a 19% decline.

Much like the chart shows, industrials and staples held up as the DOW Jones Industrial average "only" fell roughly 9%.

Value stocks had their year in the sunshine as they have finally outperformed growth. A trend we feel could continue.

|

|

|

|

|

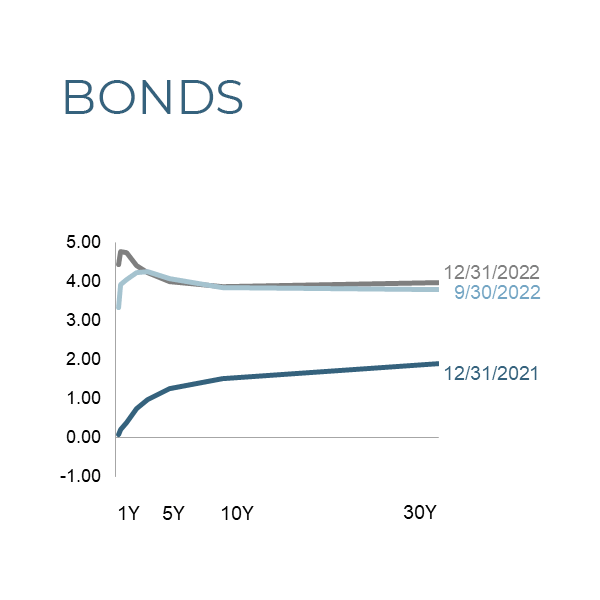

It was also a terrible year for bonds. As the yield curve shows, the shift in rates was quite large and took most bond investors by surprise.

Short term rates move up from the prior quarter, but the longer rates mostly remained flat.

As bad as stocks looked, you could have owned a thirty-year treasury bond and suffered a roughly 29% hit... in the "safety" of a government bond.

|

|

|

|

|

|

|

|

What Can Be Expected In 2023?

We expect the effects of interest rate increases to slow the economy. Inflation should moderate, which will allow Fed rate increases to end.

Our greatest concern is that the economy declines, and the Fed decides to cut rates. A rate cut could trigger animal excesses (again) which could spike inflation to higher levels than we saw in 2022.

|

We could see continued layoffs in the labor market. Currently tech is seeing the lion share, but tightening could expand beyond that sector.

Real estate will sit in no man's land as prices in core areas could remain high, sellers have not embraced reality and really don't need to sell. Rates will hurt buyers, but there really won't be any supply to absorb.

|

|

Any of the VRBO hot spots could suffer. Vacation areas as well as overly purchased communities will feel the pain.

Additionally, those who bought houses during COVID may see their equity go negative, so time will tell if those buyers have staying power.

Will there be a recession? Maybe.

|

With the hit to stocks last year, markets have already discounted a recessionary event.

If history serves, the market will start its move up by the time we are "officially" in a recession. The Fed should have a couple more hikes in their future, but the forward curve suggests easing at the end of this year.

|

|

|

|

Casting Onward

We are cautiously optimistic about this year. Now seems to be a decent entry point for stocks, although for long term investors, we feel there is never a bad time to buy stocks.

We will most likely see continued underperformance in growth sectors as rates will remain high. External situations can always change the markets' view, but our (and I believe other investors) greatest fear is another round of inflation.

We look forward to speaking to you over the next couple of weeks. We wish you and your family a happy and prosperous 2023. We stand ready to assist you in achieving your financial goals.

|

|

|

|

|

|

Have You Taken

The SpinnCycle™?

A quick reality check for your portfolio

Enter the SpinnCycle and find your SpinnScore™

|

|

|

|

|

|

Spinnaker Mobile App now Available for IOS and Android

|

|

|

|

|

Spinnaker Investment Group is a boutique, family-owned investment advisory firm that helps each investor design, implement and run a portfolio. We work directly with each client to help them realize their financial independence.

© 2023 Spinnaker Investment Group. All Rights Reserved.

Disclosures

|

GET IN TOUCH

949.396.6700

info@spinninvest.com

spinninvest.com

4100 MacArthur Blvd., Ste 120

Newport Beach, CA 92660

|

|

|

|

|

DISCLOSURES: Past performance is not a guarantee of future results. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio. Market segment (index representation) as follows: Marketwide (Russell 3000 Index), Large Cap (Russell 1000 Index), Large Value (Russell 1000 Value Index), Large Growth (Russell 1000 Growth Index), Small Cap (Russell 2000 Index), Small Value (Russell 2000 Value Index), and Small Growth (Russell 2000 Growth Index). World Market Cap represented by Russell 3000 Index, MSCI World ex USA IMI Index, and MSCI Emerging Markets IMI Index. Russell 3000 Index is used as the proxy for the US market. Dow Jones US Select REIT Index used as proxy for the US REIT market. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2023, all rights reserved. Yield curve data from Federal Reserve. State and local bonds, and the Yield to Worst are from the S&P National AMT-Free Municipal Bond Index. AAA-AA Corporates represent the ICE BofA US Corporates, AA-AAA rated. A-BBB Corporates represent the ICE BofA Corporates, BBB-A rated. Bloomberg data provided by Bloomberg. US long-term bonds, bills, inflation, and fixed income factor data © Stocks, Bonds, Bills, and Inflation (SBBI) Yearbook™, Ibbotson Associates, Chicago (annually updated work by Roger G. Ibbotson and Rex A. Sinquefield). FTSE fixed income indices © 2023 FTSE Fixed Income LLC, all rights reserved. ICE BofA index data © 2023 ICE Data Indices, LLC. S&P data © 2023 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Past performance is no guarantee of future results, and there is always the risk that an investor may lose money. Diversification neither assures a profit nor guarantees against loss in a declining market. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the securities mentioned. The information contained herein, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable. Opinions expressed herein are subject to change without notice.

|

|