| CONNECT |

|

|

|

|

|

|

|

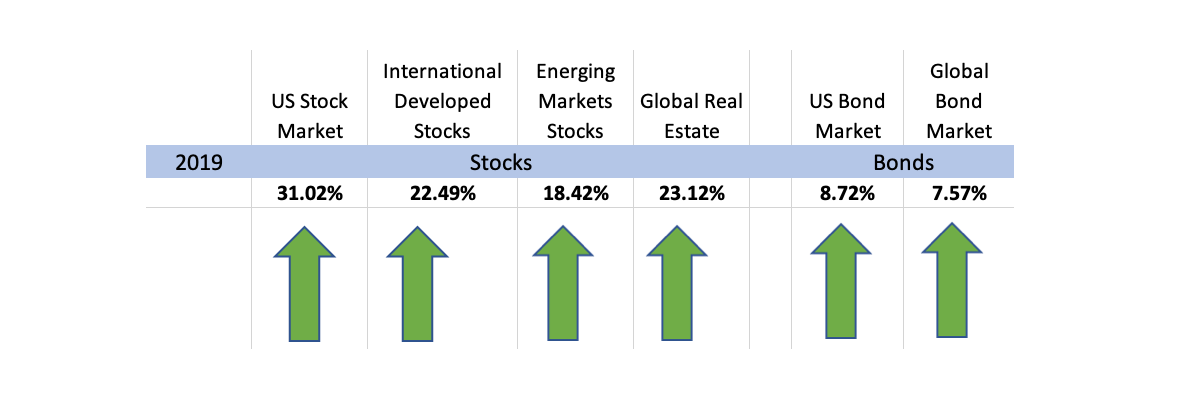

Stocks

A great year for stocks. Equity markets around the globe posted positive results. The US outperformed the non-US developed and emerging markets in 2019. Large cap stocks outperformed smaller stocks, while growth was a standout. Looking at countries, Switzerland was the best performing developed market while Greece was the top emerging market performer. Looking back at the last decade and reviewing the best performer in the S&P 1500 gives us an interesting winner. No, it is not Netflix, Apple, Cannabis, Biotech or AI... the winner is Patrick Industries. This is a company that manufactures and distributes building products and material for the RV, marine, and manufactured housing markets. Not all that exciting, but another lesson to own the market and not chase the bright light. |

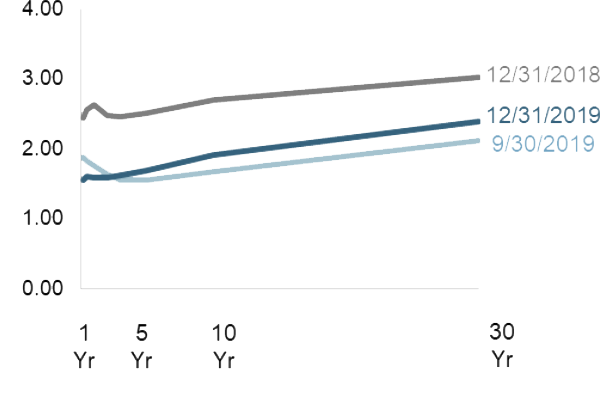

Bonds

Interest rates decreased in the US Treasury markets during 2019. The entire yield curve shifted lower, which worked well for bond investors but harmed those with savings accounts. In general, we saw the same outcome in international bonds, as most countries saw rates decrease while Japan and Germany continue to have negative nominal rates. We do not have the appetite for owning lower grade bonds at this point. At these low interest rates, corporations have been taking on debt to buy-back their shares. There has been a rise in "covenant-lite" (not a good contract) bonds that may not end well should the economy slow. The Fed has become dovish. They reversed their stance on rates and reduced the Fed Funds rate in 2019. The economy improved and recession fears evaporated, so we do not anticipate further reductions at this time. |

And?

And?

Fundamentals are solid, but that doesn't mean the markets can't sell off. American economist Hyman Minsky once said, stability breeds instability. The last few years have been pretty stable. Most bad loans and bad decisions are made during good times. Consumers have reduced their debt loads as companies have expanded theirs. Oxford Economics senior economist Lydia Boussour wrote on October 31st, "half of investment grade corporate bonds are in the lowest tier by credit rating, versus 37% in 2011. And 80% of leveraged loans are covenant-lite, versus 30% during the financial crisis. To put that into perspective, default-prone Argentina found buyers in 2017 for 100-year government bonds and Greece has buyers of their 10-year bonds that yield just over 1% per year. As investors stretch for yield, they are taking on higher levels of risk than are warranted (and compensated). |

|

|

| Spinnaker Mobile App now Available for IOS and Android |

|

|

Spinnaker Investment Group is a boutique, family-owned investment advisory firm that helps each investor design, implement and run a portfolio. We work directly with each client to help them realize their financial independence. © 2020 Spinnaker Investment Group. All Rights Reserved. Disclosures |

GET IN TOUCH

949.396.6700 info@spinninvest.com spinninvest.com 4100 MacArthur Blvd., Ste 120 Newport Beach, CA 92660 |

| DISCLOSURES: Past performance is not a guarantee of future results. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio. Market segment (index representation) as follows: US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net div.]), Emerging Markets (MSCI Emerging Markets Index [net div.]), Global Real Estate (S&P Global REIT Index [net div.]), US Bond Market (Bloomberg Barclays US Aggregate Bond Index), and Global Bond Market ex US (Bloomberg Barclays Global Aggregate ex-USD Bond Index [hedged to USD]). S&P data ® 2020 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data ® MSCI 2020, all rights reserved. Bloomberg Barclays data provided by Bloomberg. One basis point (bps) equals 0.01%. Yield curve data from Federal Reserve. State and local bonds are from the S&P National AMT-Free Municipal Bond Index. AAA-AA Corporates represent the Bank of America Merrill Lynch US Corporates, AA-AAA rated. A-BBB Corporates represent the ICE BofA Corporates, BBB-A rated. Bloomberg Barclays data provided by Bloomberg. US long-term bonds, bills, inflation, and fixed income factor data ® Stocks, Bonds, Bills, and Inflation (SBBI) Yearbook™, Ibbotson Associates, Chicago (annually updated work by Roger G. Ibbotson and Rex A. Sinquefield). FTSE fixed income indices ® 2020 FTSE Fixed Income LLC, all rights reserved. ICE BofA index data ® 2020 ICE Data Indices, LLC. S&P data ® 2020 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Diversification neither assures a profit nor guarantees against loss in a declining market. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the securities mentioned. The information contained herein, while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable. Opinions expressed herein are subject to change without notice. |